A Brutal Match Point for Domestic Filter | JD Insights

2024-11-26

Abstract:From domestic substitution to survival challenge.

Research team | JD Capital Manufacturing Investment Department

Managing Director,Xing Xiaohui xingxh@jdcapital.com

Senior Investment Manager,Xia Han xiahan@jdcapital.com

"United States has imposed four rounds of sanctions over the past two years to restrict our 5G mobile phone, so we can only use 4G now, and our 5G chips can only be used as 4G.", Yu Chengdong said at the launch of Huawei's P50 mobile phone in July 2021. Since then, the new models released by Huawei no longer show the specific network bands supported in the configuration table.

The key factor hindering Huawei's 5G mobile phone is that in addition to chip OEM, there is also a key component hidden inside the RF module: the filter, an electronic component for specific communication frequency band selection and suppression, which is part of the RF front end of the mobile phone.

Today, nearly four years have passed, Huawei Mate60 can essentially support 5G communications. However, we learned from industry research that in addition to solving baseband and chip production, Huawei can still only use a different way of solution on high-frequency filter: Either purchasing imported products from abroad, or choosing LTCC (another technical route) temporarily.

However, with the iteration of mobile communication technology, high-frequency filter is an inextricable topic to fully realize the conversion from 4G to 5G in the future, and even adapt to higher communication technology standards such as 6G. Without this component, Huawei's Kirin chip is tantamount to a trapped dragon.

In fact, in March 2021, the United States has blocked the export qualification of high-frequency filter in its sanctions against Huawei. However, we found that by this year (2024), the overall localization rate of filter is still around 10-15%, of which the localization rate of high-frequency (above 3GHz) products is almost 0.

More data showed that in the current 30 or so domestic filter manufacturers, only about 10 can really emerge in the competition. Only 4-5 domestic manufacturers can be seen in ODM and mobile phone client bidding and competition.

From the perspective of investment opportunities, the filter can be regarded as a blue ocean market with a large scale and a good substitution opportunity. But from the perspective of market performance, not only the localization rate is still low today, but the competition is fierce and low-end as well.

How difficult is it to achieve domestic substitution for filter (especially high-frequency)? In this article we will discuss about the industry and try to explore:

● What is the real challenge for domestic filter hiding behind the excitement and bubbles?

● Where is the breakthrough opportunity for Chinese filter enterprises?

● How can we find the right investment opportunity for us?

Ⅰ.What is a filter?

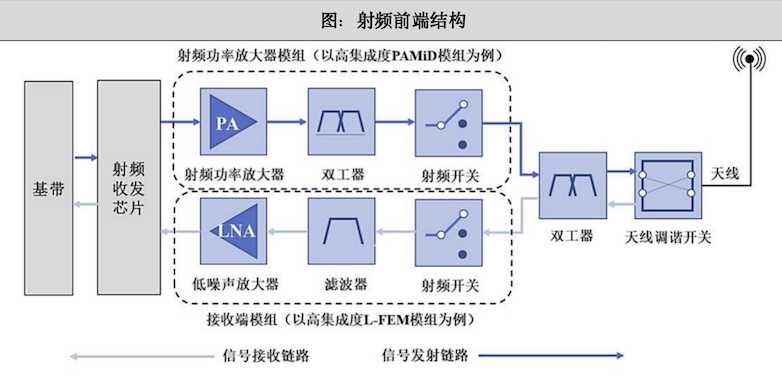

If a smart phone is regarded as a person, the RF front end is equivalent to a person's "sensory system", which is closely related to the process of receiving and transmitting information.

Usually, about 1/3 of the space on the mainboard of a mobile phone is used for the RF front end, which needs to be integrated with power amplifier (PA), low noise amplifier (LNA), filter, diplexer/duplexer (composed of 2 filters), RF switch and other components.

(Source: public data collection)

Among them, the core role of filter is to select frequency, which is to let the required frequency signal to pass through and filter out the unwanted frequency signal.

Filter is the most important discrete device in RF front end, and it is also one of the most technically difficult core components. If there is no filter, the phone is like a brick that cannot be able to accurately receive information in user’s needs.

From a market value perspective, filter is the segment in the entire RF front end with the highest value. According to Qorvo, the world's leading RF solution provider, the value proportion of filter will increase to 66% in the future.

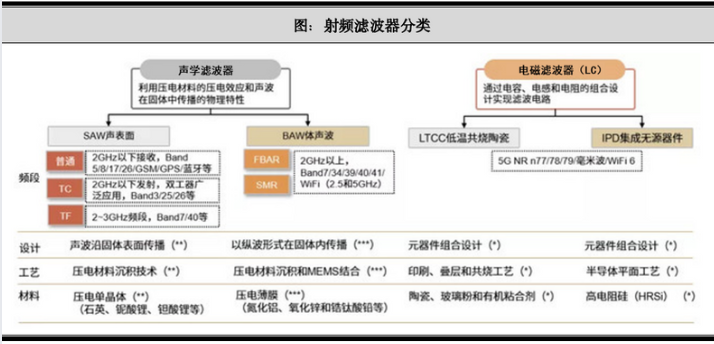

In addition to being used in the field of mobile phone, filter is also used in various communication fields such as communication base station, satellite communications and wired broadband. But this time, we mainly discuss about its use in the RF front end of mobile phone that can be divided into two categories: electromagnetic filter (mainly LC filter) and acoustic filter.

(Source: public data collection)

Taking the widely used LC filter that belong to electromagnetic filter as an example, the "LC filter" is a component composed of an inductor (L) and a capacitor (C), which can block the unnecessary frequency signal or only allow the required frequency signal to pass through. It is mainly divided into LTCC (Low Temperature Co-fired Ceramic) filter and IPD (Integrated Passive Devices) filter.

Due to poor frequency selectivity, LC filter is difficult to apply to scenarios with isolation bandwidth less than 150MHz, so the market size applied to RF field is small, which is less than 1 billion US dollars per year.

Different from LC filter, due to excellent frequency selectivity, "acoustic filter" is more suitable for RF field, and which can be divided into surface acoustic wave (SAW) filter and bulk acoustic wave (BAW) filter.

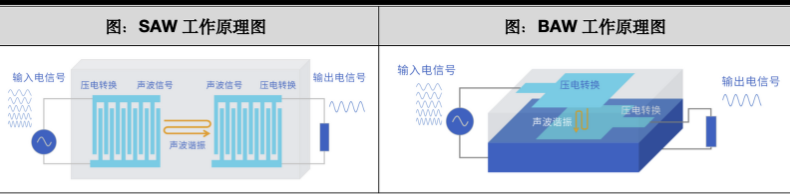

Among them, SAW filter is usually made of isopiestic electricity materials such as lithium niobate and lithium tantalate. SAW filter is a kind of special device based on the physical characteristics of piezoelectric effect and surface wave propagation. It was early used in television and other audio and visual home appliances. After the 1990s, with the development of the communications industry, the output and demand for SAW filter rose sharply, and it was widely used in mobile phone and other mobile communication terminals.

SAW has good consistency, repeatability and can be mass produced at low cost. However, due to the limitations of substrate materials (such as sound velocity, temperature excursion, etc.), Normal-SAW is mainly used for frequencies below 2GHz. At present, overseas manufacturers gradually improved the sound velocity and temperature performance of SAW substrates by improving substrate materials and increasing protective coatings, while Chinese manufacturers are relatively lagged behind in development.

BAW filter operates in the frequency range of 1.5GHz to 10GHz, and the size will shrink as the frequency increases, which is suitable for 4G and 5G communications with higher requirements.

Compared with SAW filter, BAW filter is more suitable for high frequencies. It also has the advantages of being insensitive to temperature change, low insertion loss and high out-of-band rejection.

BAW filter works in a similar way to SAW filter, except that the production process for SAW is simpler. The piezoelectric layer thickness of BAW filter for high frequency scenarios is only a few hundred nanometers, requiring the use of difficult film deposition and micro electromechanical system (MEMS), and the number of photomasks is much higher than that of SAW. The manufacturing cost is higher and the process is more complex.

(Source: public data collection)

From the perspective of product development trend, with the popularity of 5G mobile phone and the gradual commercial use of 6G frequency band, the usage of BAW will greatly increase.

However, JD Capital learned in the research that the current consensus of the industry is that the two types of filters will coexist in the market for a long time in the future, and each will play a performance advantage.

SAW is mainly used in cost sensitive products with slightly lower requirements for frequency and performance, while BAW is mainly used in high performance, high frequency and high power products.

According to the data of the industry third party company Yole, the global market size of RF filter in 2023 is about 10 billion US dollars, of which the cellular communications field (mainly mobile phone) accounts for the highest proportion, and the market size is about 8.85 billion US dollars. When divided into different types, SAW filter accounts for 61%, BAW filter accounts for 34%, and LC filter accounts for about 5%.

In terms of growth trend, JD Capital believes that with the gradual commercial use of 6G frequency band, the proportion of BAW will gradually increase and is expected to exceed the market share of SAW.

Therefore, in the long run, the growth rate of BAW filter will be faster than the growth rate of the entire consumer electronics, especially the mobile phone market.

Ⅱ.A start up industry hard as hell?

As an industry with large volume, strong certainty of downstream market demand and high product value, why domestic filter is still in chaos today? How hard is it to produce a filter?

From the technical difficulty perspective, inside the entire RF front end, the difficulty of switches and LNA is low, PA is relatively difficult, and the filter is the most difficult.

At present, domestic enterprises have basically completed domestic substitution in devices such as switches, LNA and PA, and some substitution has also been made in middle and low frequency SAW, while the substitution in high frequency BAW filter has not yet been achieved.

In 2021, industry data showed that the domestic PA procurement proportion of the top ten domestic mobile phone manufacturers has reached 30%, while the localization rate of RF filter in 2024 is expected to be about 15%, of which is mainly SAW filter. High frequency BAW applied to the mobile phone field has not yet been shipped by domestic manufacturers.

Even if domestic substitution has partly been achieved in SAW filter, the substrate material used in production is still dependent on import at this stage.

According to the "2022 Annual Non-public Offering A-Share Plan" released by domestic lithium niobate/lithium tantalate crystal leader TDG, it shows that at this stage, the main country that can produce the related substrate materials internationally is Japan. In the global market, four Japanese manufacturers (ShinEtsu, Sumitomo, Xiaochi and Shanshou) account for more than 90% of the market share.

The difficulty of producing BAW filter is mainly reflected in two aspects:

1. The process complexity is extremely high to accurately control the film thickness;

2. To bypass the structural patent restrictions of foreign manufacturers.

At the technical level, BAW is mainly used in the field of high frequency, and higher frequency requires smaller film thickness with weaker piezoelectric characteristics, which contributed to a higher defect proportion of the polycrystalline piezoelectric layer, and a more difficult control in the film quality, consistency and stress. The difficulty of the production process increases exponentially.

This is like calculating the landing time of a solid iron ball. As long as the gravity of the iron ball is considered, other factors can be ignored, so it is relatively easy. However, it is more difficult to consider complex factors such as the environment and wind speed in calculating the landing time of a feather or a piece of paper.

In fact, whether it is SAW or BAW, the production of them both need special techniques with industrial know-hows. According to the industry research of JD Capital, only some domestic head manufacturers can achieve about 90% of the level of foreign manufacturers in the performance of filter discrete devices. The gap is even greater at the module level.

More importantly, at the manufacturing level, the production of filter needs not only the control on variable factors, but also maintain product consistency while achieving mass production.

Moreover, due to the uncertainty of product design and process, it is necessary to explore and revise repeatedly. However, compared with the shipments of other chips, the amount of filter is not large, which contributed to a low cooperation willing of the OEMs. Therefore, most of the industry giants adopted the IDM (Integration of Design and Manufacture) mode. A close combination of design and process is the only way to make products more stable, faster iterative, and less costly.

But this also determines that the filter industry is naturally difficult: large investment, heavy assets, and ultimately must be in a situation of oligopoly competition.

Another key difficulty is patent restrictions.

Invention patents involved in the design, manufacture, packaging and testing of filter. According to Yole statistics, since 1970, there have been more than 8000 invention patents related to filter in the world, including more than 6500 SAW filter patents and about 1700 BAW filter patents, which are almost monopolized by overseas giants.

At present, the core patents of BAW filter are valid for the period of 2029-2034. Although the core patents of ordinary SAW have expired, there may still be a risk of infringement of foreign patents in order to achieve a good filter performance.

Take the patent dispute between HD Shoulder and Murata as an example, the patent that Murata sued was not the core patent of SAW, and the dispute was ended in a reconciliation.

Therefore, in the view of JD Capital, domestic manufacturers must start from underlying research and development to avoid patent problems in the short term. Even adopting the traditional technical route, it is still possible for chances to bypass the core patents through forward research and development.

However, in the long run, only breaking through on substrate materials, changing the existing material system or starting a new technical route can solve the patent restrictions fundamentally.

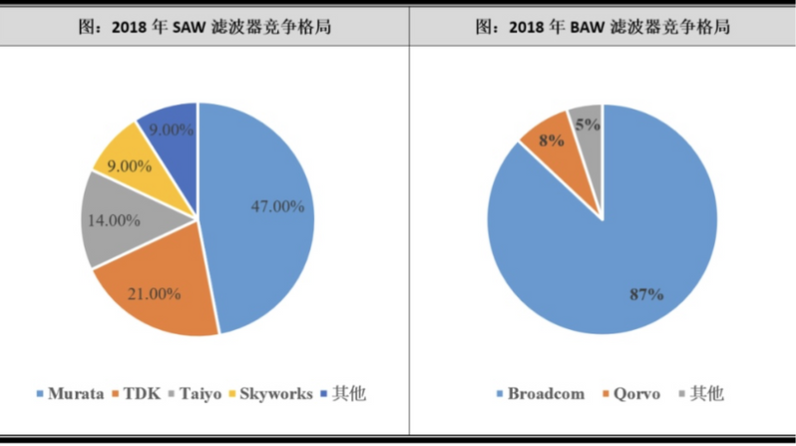

In fact, today's patent landscape also reflects the filter market structure. From the perspective of patent owners, SAW filter leading company Murata has more than 1000 related patents, and BAW filter leading company Broadcom has about 300 related patents.

From the perspective of the competitive pattern of filter, the entire industry is mainly monopolized by American and Japanese companies with high concentration and constant advantages.

China is currently playing a role as a filter consumer giant. The overall strength of the domestic filter manufacturers is weak. The product output cannot meet domestic demand and is long depended on import. China's SAW filter production accounts for only about 3% of the global market, while the proportion of high frequency BAW filter is basically 0%.

(Source: public data collection)

Ⅲ.Knockout has begun, reshuffle is underway

In 2020, news reports showed that the gross profit rate of the entire domestic RF front end was once as low as 20%. But at that time, most of the startup enterprises still have an ideal to fight against a number of high-end overseas enterprises.

However, several years later, their products still cannot compete with domestic leading enterprises. As a result, selling goods at a lower price has gradually become a lifesaver for startups in this market in recent years.

What is even crueler is that with the continuous decline of the consumer electronics market, cancellation on orders prevailed and the reduction on inventory made the market even worse.

However, in the view of JD Capital, the declination of consumer electronics market is only the external reason resulting in low and medium frequency filters entering the stalling market. What’s more important is the internal reason: Domestic filter manufacturers only focused on the competition in low-end low and medium frequency field, which contributed to severe homogenization in products, while no breakthrough has been made in the field of high frequency, therefore domestic filter manufacturers can only compete on product price.

Taking WIFI2.4G filter as an example, the price in 2023 is about 0.2 yuan/piece and the price dropped by 50% in 2024.

By industry research, JD Capital also learned that the gross profit rate of foreign filter manufacturers is generally more than 30%-40%. Due to the high operating costs of foreign manufacturers, it is difficult to cover the products under 30% of gross profit rate.

As for domestic filter manufacturers, most SAW filters are in a stage of negative gross profit except for a few leading enterprises with positive profits; BAW filter manufacturers generally sell at a loss.

However, unlike low-end low and medium frequency SAW filter, JD Capital believes that the main reason for domestic high frequency BAW filter manufacturers currently shipping at a loss is that:

1. The mass-produced models for BAW filter manufacturers currently concentrated in B40/N41/WIFI2.4. Although the amount of such filters is large, the technical difficulty is low. What’s more, such filters need to compete with SAW filters. Although the price is consistent with SAW filters, the cost is much higher than SAW, which resulting in the negative gross profit rate;

2. There are also some manufacturers taking the initiative of strategic losses aim to accumulate shipments in order to obtain the qualification of supply from head mobile phone manufacturers. After all, a lower price is the best way to reach customers;

3. The main customers for domestic BAW filter manufacturers are currently concentrated in the field of Internet of Things and ODM with a sensitive feeling to price. Therefore, the product pricing has a discount of about 50% compared with foreign manufacturers.

In fact, JD Capital found in research that the knockout round of domestic filter has begun, and the industry reshuffle is taking place this year.

How can domestic manufacturers climb out of the mire and get rid of the dilemma of negative gross profit in a market that few manufacturers make profit while most manufacturers bear losses?

From a pragmatic point of view, JD Capital believes that:

1. For SAW filter manufacturers that using existing material systems and production processes: The problem for them is how to make positive gross profit products and how to improve product performance, rather than unthinkingly compete on product price and costs. Under the premise that main raw materials and equipment rely on import, it is difficult for them to achieve cost advantage.

2. For the filter manufacturers using new material systems and new processes: The problem for them is how to quickly achieve industrialization and acquire recognition from industry benchmarking customers, so that the industry can realize the potential of the new routes.Of course, such manufacturers are mostly in the early stage and in lack of hematopoietic ability, but they also need to seize every opportunity in finance to ensure cash flow and take strict control on costs.

3. For domestic BAW filter enterprises: The current situation is quite awkward, low-band products cannot compete with SAW and high-band products under Sub6GHz faces LTCC/IPD competition. The market scale that can be reached is small. However, in the future, with the arrival of 6G and the increase in the penetration rate of WIFI6E/WIFI7, the isolation band among high frequency bands will be reduced, which will contribute to the situation that traditional LTCC/IPD cannot meet requirements, and the need for BAW will be highlighted. Therefore, the problem for BAW enterprises should be research and development of high-frequency and high-bandwidth products in rigid demand, and gradually reduce the volume of low-frequency products with low margin or negative gross margin. Under the current situation that it is difficult to enter the head flagship models in the short term, domestic BAW enterprises can focus on the development of WIFI routers, CPE and high-frequency BAW products for military industry, laying out on the areas that SAW and LTCC/IPD cannot address.

The business relied on burning of money is doomed to be unsustainable. With the intensification of market reshuffle, the vicious competition with the help of financed funds will be eased.

In the future, manufacturers without self-built factories, sufficient cash reserves and differentiated products will inevitably be knocked out by the market.

Ⅲ.Knockout has begun, reshuffle is underway

In 2020, news reports showed that the gross profit rate of the entire domestic RF front end was once as low as 20%. But at that time, most of the startup enterprises still have an ideal to fight against a number of high-end overseas enterprises.

However, several years later, their products still cannot compete with domestic leading enterprises. As a result, selling goods at a lower price has gradually become a lifesaver for startups in this market in recent years.

What is even crueler is that with the continuous decline of the consumer electronics market, cancellation on orders prevailed and the reduction on inventory made the market even worse.

However, in the view of JD Capital, the declination of consumer electronics market is only the external reason resulting in low and medium frequency filters entering the stalling market. What’s more important is the internal reason: Domestic filter manufacturers only focused on the competition in low-end low and medium frequency field, which contributed to severe homogenization in products, while no breakthrough has been made in the field of high frequency, therefore domestic filter manufacturers can only compete on product price.

Taking WIFI2.4G filter as an example, the price in 2023 is about 0.2 yuan/piece and the price dropped by 50% in 2024.

By industry research, JD Capital also learned that the gross profit rate of foreign filter manufacturers is generally more than 30%-40%. Due to the high operating costs of foreign manufacturers, it is difficult to cover the products under 30% of gross profit rate.

As for domestic filter manufacturers, most SAW filters are in a stage of negative gross profit except for a few leading enterprises with positive profits; BAW filter manufacturers generally sell at a loss.

However, unlike low-end low and medium frequency SAW filter, JD Capital believes that the main reason for domestic high frequency BAW filter manufacturers currently shipping at a loss is that:

1. The mass-produced models for BAW filter manufacturers currently concentrated in B40/N41/WIFI2.4. Although the amount of such filters is large, the technical difficulty is low. What’s more, such filters need to compete with SAW filters. Although the price is consistent with SAW filters, the cost is much higher than SAW, which resulting in the negative gross profit rate;

2. There are also some manufacturers taking the initiative of strategic losses aim to accumulate shipments in order to obtain the qualification of supply from head mobile phone manufacturers. After all, a lower price is the best way to reach customers;

3. The main customers for domestic BAW filter manufacturers are currently concentrated in the field of Internet of Things and ODM with a sensitive feeling to price. Therefore, the product pricing has a discount of about 50% compared with foreign manufacturers.

In fact, JD Capital found in research that the knockout round of domestic filter has begun, and the industry reshuffle is taking place this year.

How can domestic manufacturers climb out of the mire and get rid of the dilemma of negative gross profit in a market that few manufacturers make profit while most manufacturers bear losses?

From a pragmatic point of view, JD Capital believes that:

1. For SAW filter manufacturers that using existing material systems and production processes: The problem for them is how to make positive gross profit products and how to improve product performance, rather than unthinkingly compete on product price and costs. Under the premise that main raw materials and equipment rely on import, it is difficult for them to achieve cost advantage.

2. For the filter manufacturers using new material systems and new processes: The problem for them is how to quickly achieve industrialization and acquire recognition from industry benchmarking customers, so that the industry can realize the potential of the new routes.Of course, such manufacturers are mostly in the early stage and in lack of hematopoietic ability, but they also need to seize every opportunity in finance to ensure cash flow and take strict control on costs.

3. For domestic BAW filter enterprises: The current situation is quite awkward, low-band products cannot compete with SAW and high-band products under Sub6GHz faces LTCC/IPD competition. The market scale that can be reached is small. However, in the future, with the arrival of 6G and the increase in the penetration rate of WIFI6E/WIFI7, the isolation band among high frequency bands will be reduced, which will contribute to the situation that traditional LTCC/IPD cannot meet requirements, and the need for BAW will be highlighted. Therefore, the problem for BAW enterprises should be research and development of high-frequency and high-bandwidth products in rigid demand, and gradually reduce the volume of low-frequency products with low margin or negative gross margin. Under the current situation that it is difficult to enter the head flagship models in the short term, domestic BAW enterprises can focus on the development of WIFI routers, CPE and high-frequency BAW products for military industry, laying out on the areas that SAW and LTCC/IPD cannot address.

The business relied on burning of money is doomed to be unsustainable. With the intensification of market reshuffle, the vicious competition with the help of financed funds will be eased.

In the future, manufacturers without self-built factories, sufficient cash reserves and differentiated products will inevitably be knocked out by the market.

Ⅳ.Is there still a chance of breakthrough for domestic filter?

Ⅳ.Is there still a chance of breakthrough for domestic filter?

In the long run, domestic filter enterprises must establish differentiated innovation capabilities first to completely achieve industrial breakthrough.

Rf filter is a combination of material, process and design. All these factors are indispensable. If domestic manufacturers only rely on the existing material system and technical route, whether it is SAW or BAW, it is difficult for them to surpass the existing overseas counterparts in the short and medium term. Therefore, domestic manufacturers must take differentiated route.

Murata, the leading SAW filter company, has been deeply engaged in this field for many years and controlled the core multi-layer substrate technology of high-end TF-SAW, which is difficult for domestic manufacturers to surpass in performance. Foreign BAW filter manufacturers have a long time of accumulation in the field of low and medium frequency, so it is also hard for domestic manufacturers to surpass.

However, in the high frequency field, JD Capital believes that the possibility for domestic BAW filter to catch up is relatively large, especially for the 30% above scandium doping technology that home and abroad are basically at the same starting line.

In this year's research, JD Capital found that there are already domestic manufacturers trying to produce high frequency RF filters with different material systems. Although they have not achieved mass shipment and yet to be verified by the market, it is worth looking forward to.

Secondly, take the IDM mode.

In the early days, subjected to financial capacity, many filter enterprises took Fabless or Fablite mode that highlight on the ability of design to enter the market and search for OEM. However, in order to maintain competitiveness, JD Capital believes that IDM is an unavoidable mode for filter enterprises and it is also a must for them to be recognized by head customers.

Since the RF filter requires characteristic process, only when the production side is closely combined with the design side can the needs from design side be better understood, so as to develop the corresponding process and produce high yield products. What’s more, the IDM mode can open up design and production, which is crucial for rapid development and iteration of products.

In general, the production cycle of OEM is significantly higher than that of the IDM. Taking BAW filter as an example, the production cycle of wafers and packages for OEM is 2-3 months, while for IDM, it can be controlled within 1 month. Moreover, the cooperation of OEM to research and development is weak, resulting in a lower speed of product iteration than IDM.

In terms of cost, although the initial investment of IDM is large, the unit cost of the product is low and the gross profit can be gradually recovered.

Today, in order to be eligible to supply for flagship models, filter enterprises are required by head mobile phone manufacturers to have their own factories to ensure a stable supply of products. Therefore, domestic head filter manufacturers are building their own factories and switching to IDM mode.

Thirdly, to achieve bulk supply for mobile phone manufacturers and to participate in the flagship model competition.

At present, domestic mobile phone manufacturers have formed a situation of top four for Huawei, Xiaomi, OPPO and vivo.

According to the global smartphone shipment data in 2023, Apple and Samsung accounted for 20.10% and 19.40% of the global share, totaling 39.5%. Xiaomi, OPPO and Transsion together account for 29.4%. Chinese enterprises (Xiaomi, OPPO, vivo, Transsion, Honor, realme, moto and Huawei) are expected to account for more than 50% of the total.

Therefore, domestic filter enterprises could have a chance to compete with overseas giants only if recognized by the "top four". Meanwhile, only by participating in the competition of flagship mobile phones can domestic filter enterprises have the opportunity to obtain more profits.

The prerequisite for filter enterprises to enter mobile phone manufacturers is to achieve bulk shipments for ODM. Taking a mobile phone manufacturer as an example, before the filter enterprise can supply for its flagship model, it firstly requires the filter enterprise to achieve shipment for its non-main models through ODM, and secondly requires the filter enterprise to accumulate tens of millions of ODM shipments of a single filter model.

ODMs are mainly OEM for non-main models with lower price. They are sensitive to filter price. Therefore, ODMs have strong incentive to introduce domestic filter suppliers. The threshold to enter ODM is lower than that of mobile phone manufacturers.

Finally, modularization is the inevitable trend in the future.

Taking Huawei, Xiaomi, OPPO and vivo as examples, thousand-yuan models have begun to use RF modules. Although separate devices will continue to exist, the proportion will continue to decrease. With the gradual breakthrough of domestic manufacturers, only with the shipping capacity of high gross profit products such as modularized devices can domestic manufacturers gradually get rid of the dilemma of negative gross profit.

Of course, the current situation is the long time supply time period of self-developed modules and the incomplete domestic filter models. Most enterprises can only cover 4G band and are able to supply 4G or 3G modules, but they are not able to supply 5G modules. At the same time, it is also necessary for self-developed modules to have technical abilities of PA, LNA and switch, which require difficult technology and long verification cycle.

Therefore, JD Capital believes that a more pragmatic solution is to establish a strategic partnership and combine with the existing RF front end module enterprises in order to provide filters by filter enterprises and integrate modules by module manufacturers. This is a more realistic way for BAW filter startups in the short term.

Self-modeling puts forward higher requirements on the technical ability of filter enterprises, but in the medium and long term, this is the ability that filter enterprises must possess.

At present, JD Capital found that some long established SAW filter enterprises have achieved volume production and shipment of self-produced modules in the market, but BAW filter manufacturers have not achieved self-developed module shipment records for the time being.

In terms of specific investment opportunities, JD Capital believes that domestic filters that possess the ability of cost advantages, volume production and shipment on high-frequency products (or differentiated products), core products certified by head phone manufacturers are still ideal investment targets.

From the perspective different technical routes, JD Capital believes that there still have investment opportunities in both SAW and BAW in the future.

Among them, domestic manufacturers in the field of BAW filter must achieve breakthrough in high-frequency BAW, high-power BAW, high-bandwidth BAW, quadruplex and some technically difficult diplexers to get rid of the fierce competition, providing differentiated products to the market. At the same time, they need to reduce costs continuously by process improvement, seeking cost advantages against peers and foreign competitors.

Although the competition in SAW filter is fierce, the market space that can be reached is larger than that of BAW for domestic manufacturers. The difference is that among SAW manufacturers under traditional material system, a small number of head manufacturers that have successful entered into the supply chain of Huawei, Xiaomi, OPPO and vivo have basically landed.

However, as for new SAW manufacturers, it is difficult for them to make breakthrough if they still use traditional material system and the chance for them is slim. New SAW manufacturers must seek new material system or technical route to go beyond from cost or performance side to grasp opportunities.