On the eve of mass production, humanoid robots start supply chain positioning war | JD Insights

2025-09-09

(Generated by ChatGPT)

Abstract:Build a strong supply chain that is "usable, sufficient, cheap and mass-produced"

Research Team | JD capital Manufacturing Investment Department

Director General Manager, Xing Xiaohui xingxh@jdcapital.com

Senior Investment Manager, Xia Han xiahan@jdcapital.com

In the summer of 2025, the tech world was permeated with a familiar mix of excitement and anxiety. The stars were no longer smartphones or electric cars, but humanoid robots called "Iron Man" . Tesla's Optimus moved nimbly through factory floors, awkwardly tightening screws; while products from companies like China's Yushu Technology and Zhiyuan Robotics could already perform complex tasks such as backflips and parcel sorting.

Is this wave the prelude to a new technological revolution, or just another bubble of AI? Are we on the eve of the release of the "iPhone 1" of humanoid robots?

The answer may be more complicated than you think.

JD Capital observes that while we stand on the brink of a revolutionary product's emergence, this "iPhone 1" still faces challenges including high costs and reliability concerns. It is more like a signal, announcing the opening of a brand-new track. Within this emerging arena, a supply chain war that will determine the dominance of trillion-dollar industries has quietly begun.

Unlike the path of companies such as Figure AI in the United States, which are driven by AI and software algorithms, China's humanoid robot industry exhibits stronger characteristics of "hardware first" and "scenario-driven".

We believe this is not a case of overtaking on a curve, but an evolutionary path rooted in the unique soil of China. In this race, whoever first builds a robust supply chain that is "usable, sufficient, affordable, and mass-producible" will likely hold the key to defining the next era.

Ⅰ.Fire or Eve? China chose a more "hard" path

The year 2025 marks a critical period for China's humanoid robots to transition from technical validation to commercialization, truly becoming the "first year of mass production". The core indicator of this judgment is that leading products represented by Tesla's Optimus have largely completed the closed loop of basic functions such as walking and grasping, and have begun small-scale pilot applications in industrial scenarios. This is akin to the first-generation iPhone, which, despite its imperfections, demonstrated a brand-new possibility to the world.

The underlying driving force of this boom is the deep coupling of multiple factors. JD Capital believes that if weights must be assigned, then:

● Breakthroughs in embodied intelligence technology: This serves as the core engine. The emergence of large models has resolved the closed-loop challenge for robots transitioning from "understanding the world" to "actively shaping it", enabling them to evolve from mere "machines" executing preset programs into intelligent agents capable of comprehension, decision-making, and interaction.

● Tesla's "Catfish Effect": With its aggressive mass production plan (targeting 50,000 units by 2026) and formidable supply chain integration capabilities, Musk and his Optimus have stirred the entire industry like a catfish. Not only has it validated the feasibility of commercialization, but more importantly, it has compelled China's supply chain to rapidly iterate in alignment with its ambitious mass production goals. This has given tremendous confidence to the domestic industrial chain.

● National policy support: In October 2023, China's Ministry of Industry and Information Technology issued the "Guidelines for the Innovative Development of Humanoid Robots", setting a clear timeline for industrial development at the national level. Local governments in Shanghai, Shenzhen, Beijing, Shandong, and other regions have led in formulating detailed action plans. Industrial funds worth billions in Beijing and Shenzhen have provided substantial financial support for the transition of technologies from laboratories to factories. Cities such as Shanghai and Hangzhou have successively introduced specific incentive policies to promote the application of humanoid robots, injecting strong momentum into their widespread adoption.

Interestingly, in this global race, China and the US are taking two very different paths.

In the United States, represented by Figure and Tesla Optimus, there is a stronger emphasis on "software-defined hardware" with AI algorithms taking the lead, aiming to first create a "super brain" for robots. In contrast, China tends to adopt a "hardware iteration-driven software development" approach, continuously optimizing the "body" of robots and refining their "brain" through practical application scenarios.

JD Capital believes that the essential reason for this difference lies in the distinct technological advantages of China and the United States. The United States leads the world in AI algorithms and software ecosystems, while China possesses the most powerful and comprehensive manufacturing foundation and electronic supply chain in the world.

Will this lead to two very different industrial endings? Our answer is "no".

Ultimately, software and hardware must develop in tandem, converging through different paths. However, the differences in approaches determine the fundamental divergence in phased priorities and investment logic. For China's component companies, this means they must consider costs and mass production earlier and more deeply, rather than merely pursuing the "ceiling" of performance.

In the view of JD Capital, "usable, sufficient, cheap and mass production" are the twelve words that are the core of the current investment logic of China's humanoid robot supply chain.

While we focus on extreme performance, we also pay more attention to the enterprise's ability to quickly reduce costs, scale up quickly, and deeply bind downstream key customers under the scenario of meeting existing needs.

Ⅱ."Gold Mining" logic: Why bet heavily on upstream and what to dig for upstream?

Facing the highly uncertain competition pattern of downstream machine manufacturers—— who will win in the end is a huge variable—— JD Capital chooses to move upstream at this stage, to be that "spear seller" and "arms dealer".

In the long run, complete machine factories and components have high investment value. But in the short to medium term, components and modules are more certain and relatively low risk. In fact, this is the general consensus of the industry.

However, the choice of JD Capital to invest heavily in upstream components and modules is not a simple defensive strategy, but based on a deep insight into the value distribution of the industrial chain:

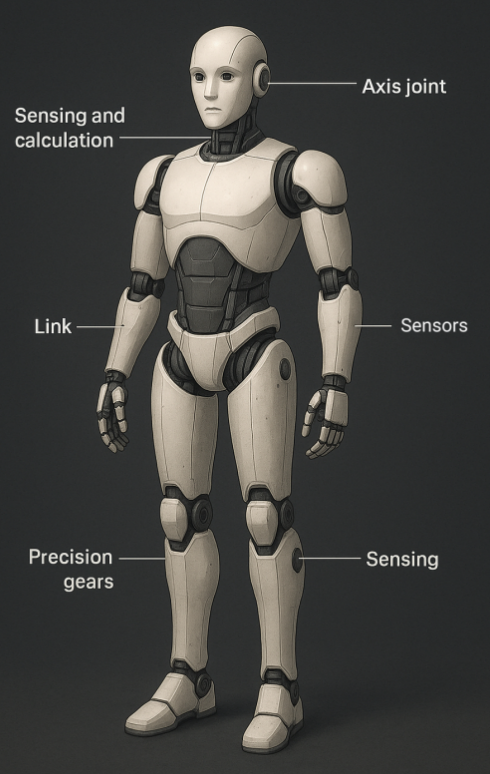

● High proportion of value: In the hardware cost of humanoid robots, the core components such as reducer, screw rod, sensor and motor account for more than 60%. This is the most intensive part of value.

● Technological iteration dominates: The upper limit of machine performance is determined by upstream components. For a robot's body to evolve, it must first have stronger "joints" and "nerve endings".

● Multi-customer coverage and anti-cyclical capability: A good parts company can serve all players such as Tesla, Zhiyuan, Yushu at the same time. No matter who dominates the downstream, the demand for core parts is rigid.

● Pioneering scale: Compared with complex complete machines, standardized core components are easier to achieve large-scale production and enjoy the dividends of industrial explosion first.

(Generated by ChatGPT)

So if you take a humanoid robot apart into a "human", where exactly is the gold mine of investment buried?

JD Capital's answer is "limbs" (joints/executors) and a perception layer (sensors) associated with the function of the "cerebellum".

We believe that the "brain" (AI algorithms and chips) is a battleground for tech giants, and OEMs will never hand over the "soul" to others, so there are not many investment opportunities in the primary market. The technical barriers of the "body" (structural components) are relatively low and the commercial value is limited.

As a result, the "limbs" and "brain" have become high-value areas. Joints are the core of cost, the bottleneck of performance, and the difficulty of mass production; while the perception layer, especially force control and touch, is the key to achieve safe and dexterous interaction of robots, and the technical barriers are higher.

In terms of investment preference, the current focus of JD Capital is to bet on "hidden champions" that are extremely good at a single link, rather than platform companies.

As the technological landscape remains fragmented with multiple competing approaches, platform-based companies face excessive risks. In contrast, "hidden champions" establish deep moats in specialized vertical sectors, becoming indispensable components of industrial ecosystems. The true value of platform companies will only emerge when these industries reach maturity.

Ⅲ.Core components in depth: The war between joints, hands and sensors

1, Core joints/executors: The "deadly" balance between cost and performance

Joints are one of the most expensive parts in humanoid robots, and also the most important part of the whole machine cost reduction. At present, there are various technical routes in the market, such as:

(1)"Motor + reducer" drive scheme

● High precision scheme: with harmonic reducer as the core, this scheme has high cost and slightly poor impact resistance, but it has high precision, the most mature technology and relatively perfect supply chain. It is expected to be the mainstream in the next 5-10 years, and is mainly used in the upper limb that needs fine operation.

● Low precision scheme: with planetary reducer as the core, this scheme has poor accuracy, low cost and strong impact resistance. It is mainly used in lower limbs and parts with slightly lower precision requirements.

(2)Direct motor drive scheme

● High precision scheme: with high resolution encoder and force control algorithm, the positioning error is small, the dynamic response is fast, and the long-term potential is huge. It can simplify the structure and improve the bandwidth, but it is difficult to become the main force in the short term due to the current motor technology, thermal management and cost.

● Low precision scheme: simple brushless direct drive motor, no high precision sensing or control, large error, only used for auxiliary joints without precision requirements (such as toy robot joints).

In different routes, what is the core contradiction at this stage? It is cost reduction.

Which is more cost-effective in the current situation, a solution that can reduce the cost by 50% but has a performance score of 80, or a solution with a performance score of 100 but a high cost? Our answer is the former.

In current market scenarios, there's no urgent need for a product with exceptional performance. The key to early-stage scalability lies in rapid cost reduction. The true value of investment depends on achieving "adequate performance + disruptive cost structure + mass production capability".

This implies that for joint suppliers, the market will not be dominated by a single dominant player. Instead, multiple solutions will coexist and be flexibly combined based on the specific requirements of different robot components, cost objectives, and control complexity. The company that first achieves the optimal balance between cost and performance in a particular technical path will gain a competitive edge.

(Generated by ChatGPT)

2, Dexterous hands and sensors: The "last kilometer" to commercialization

In addition to walking ability, the ability to operate the "hand" is considered to be the key to the commercialization of humanoid robots.

In industrial applications, the hands are what truly define humanoid robots 'core value. While wheels could handle basic movement, the real game-changer lies in their ability to perform manual tasks – especially those automation systems can't handle. From tightening screws and wiring harnesses in tight spaces to applying adhesive tapes and assembling components, these precision operations that once required skilled workers now showcase humanoid robots' unique advantages.

This is precisely why dexterous hands have become the "Mount Everest" of technical barriers and cost control. As highly integrated precision modules, they densely integrate expensive components such as micro motors, precision reducers, lead screws, precision gears, connecting rods (or tendons), and various sensors. Currently, mainstream dexterous hands in the industry cost over tens of thousands of yuan each. Their core competitive advantage lies in:

● Hardware and Cost: In the short term, this remains the biggest challenge. On the design front, the technical solutions for dexterous hand have yet to converge, limiting upstream component mass production capabilities. On the cost side, core components such as motors, lead screws, tension ropes, reducers, encoders, and controllers are constrained by manufacturing processes and batch production capacity, resulting in high costs with significant long-term potential for cost reduction.

● Algorithm and Integration: In the medium to long term, as hardware technology matures, the "hand-eye-brain" integrated control algorithm will become a true value proposition. While humanoid robots currently struggle with high-precision hand movements, requiring substantial data accumulation to enable effective motion command generation, the current focus should be on algorithm optimization rather than mere data accumulation. This demands large-scale models specifically optimized for humanoid robots' motion characteristics and perceptual patterns to ensure better adaptability.

In the perception layer, the six-axis force sensor stands as the crown jewel. It enables robots to detect forces in X, Y, and Z directions along with corresponding torque measurements on each axis, forming the core of precision force control. However, its localization and mass production face significant challenges, with the biggest obstacles being:

● High technical barriers: These include structural design of elastomer, assembly processes for core sensitive components (such as strain gauges), decoupling algorithms for complex environments, and high-precision automated calibration. This requires deep interdisciplinary integration across mechanics, materials science, electronics, and other fields, along with extensive engineering experience. Notably, the decoupling algorithm stands as the core of the core, making it particularly challenging to replicate in the short term.

● Low degree of automation: the installation of strain sheet, internal wiring debugging and calibration of six-dimensional force sensor are mainly manual assembly at present, and the difficulty of automation is high, resulting in high production cost.

Up to now, the original market size of six-axis force sensors has been relatively small, dominated by international brands such as ATI (USA) and Kistler (Switzerland). Although a number of domestic startups have emerged in China, their technological capabilities and market progress are not significantly different, all remaining at the "sample submission" and "small batch" stage.

In the view of JD Capital, the next challenge for China's six-axis force sensor suppliers is to see who can establish cooperation with genuine whole-machine giants to improve technical stability and shipment volume.

We conclude that for startups in the six-dimensional force sensor space to succeed in this replacement war, they must have several characteristics: deep technical background, strong market development capabilities (access to the supply chain of top customers), excellent engineering and cost reduction capabilities, and rapid response to collaborative iterations with customers.

Ⅳ.Investment Philosophy: How to bet in no man's land?

In the early stages of an industry without stable revenue streams or mature products, traditional valuation models (Price-to-earnings ratios, P/E) become completely ineffective. For investors developing robotic components, this resembles a high-stakes gamble. So how do private equity firms build their own valuation models to balance high valuations with high risks?

JD Capital believes that an ideal investment target must have the following key elements:

● The irreplaceability and high barriers of technical solutions: It is necessary to ensure that the invested technology route will not be easily overturned in the future. The product combining software and hardware has a deeper moat because its algorithm is difficult to be copied.

● Huge market space: look for those components that account for a high proportion of the value in the robot body, but have a small original market space. Such targets will benefit the most from the industrial explosion and have huge growth elasticity.

● Top-notch and complementary founder team: This is the most important of all elements. The team should not only have a deep technical background, but also have a strong engineering, commercial orientation and cost awareness.

● Good competition: it is best that there are no strong listed competitors in the segment.

In terms of valuation, we use the logic of "scenario reverse and cash flow discounting": how big the whole market will be in the future, how much share this component can take, and how much cake it can get.

This investment is essentially a bet on the future, with the key lying in the correctness of the technological roadmap and the team's execution. But ultimately, it is a bet on China's future in the new global tech race.

Ⅴ.Endgame: Who will define the next era?

When will the "iPhone moment" of China's humanoid robot industry—— that benchmark product capable of entering thousands of industries—— arrive? Industry forecasts are:

● The "iPhone 1" moment (the first tipping point product) —— is likely to occur around 2028-2030, marked by the realization of large-scale profits for robots in two or three core industrial scenarios (such as automobile manufacturing, warehousing and logistics).

● The iPhone 4 moment (mass adoption) —— A truly universal, home-ready benchmark will take longer, probably after 2035.

Prior to this, JD Capital identified several critical milestones the industry must achieve: reducing core component costs to a tipping point, attaining breakthroughs in embodied intelligence, attaining scale profitability in key application scenarios, and establishing robust supply chains. Currently, the primary bottlenecks constraining industry growth are cost and technological limitations in the short term, while AI's generalization capabilities will be crucial in the medium term.

Ten years from now, when we look back at today, what will ultimately determine the global status of China's humanoid robot industry? The answer from JD Capital is the synergy of three factors: market size, manufacturing costs, and core technologies.

But in the long run, China's humanoid robots will inevitably lead global development and give birth to world-class, irreplaceable companies. This is because China possesses the world's largest application market and the strongest manufacturing cost advantage, which serves as both the "fertile soil" and "foundation" for technological development.

In the view of JD Capital, we can first rely on these two points to quickly increase volume and occupy the market, and then use the market to exchange technology, feed back into research and development, and finally incubate core technologies and companies with global dominance.

After all, technology can be made up for, but the advantages of market size and manufacturing costs cannot be imitated by foreign countries.

The battle over the "Iron Man" has just begun. It concerns not only the future of an emerging industry, but also a nation's global standing in the next technological era. At this critical juncture, the decisive factors lie hidden within seemingly insignificant components: speed reducers, sensors, and screws.